Aicpa Code Of Professional Conduct Independence

Aicpa Code Of Professional Conduct

User Friendly Aicpa Code Of Ethics On Horizon

Independence Aicpa Code Of Professional Conduct Article Iv Ppt Video Online Download

Https Www Aicpa Org Content Dam Aicpa Research Standards Codeofconduct Downloadabledocuments 2014december15contentasof2015october26codeofconduct Pdf

Ethics And Professional Conduct For Cpas

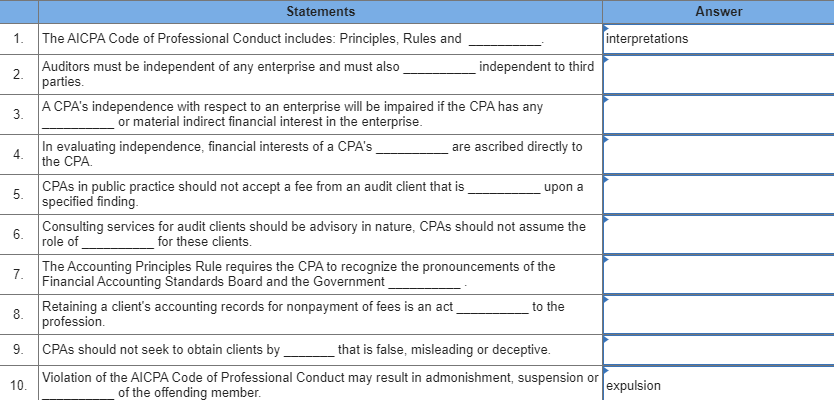

Solved Statements Answer 1 The Aicpa Code Of Professiona Chegg Com

Independence generally implies one s ability to act with integrity and exercise objectivity and professional skepticism.

Aicpa code of professional conduct independence. References changed to reflect the issuance of the aicpa code of professional conduct on january 12 1988. The aicpa and other. On june 1 2014 the aicpa issued a codification of the code s principles rules interpretations and rulings revised code. The aicpa a code of professional conduct is meant to be a general framework but there are several governing bodies that need to be considered when we approach the topic of ethics.

Pdf versions of the aicpa code of professional conduct are also available for download. The code establishes standards for auditor independence integrity and objectivity responsibilities to clients and colleagues and acts discreditable to the accounting profession. Independence requirements under the aicpa code of professional conduct the code and if applicable other rule making and standard setting bodies. 0 200 020 application of the aicpa code 01 the code of professional conduct the code was originally adopted on january 12 1988 and was periodically revised through june 1 2014.

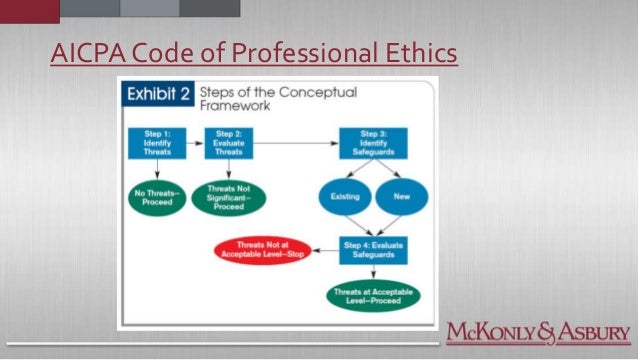

Replaces previous interpretation 101 10 the effect on independence of relationships proscribed by rule 101 and its interpretations with nonclient entities included with a member s client in the financial statements of a governmental reporting entity april 1991 effective april 30 1991. 3 not letting other people dictate or influence the cpa s judgment and professional decisions. The aicpa code of professional conduct. Conceptual framework for independence is a methodology that aids members to ascertain whether independence has been impaired due to identifiable threats.

Independence generally implies one s ability to act with integrity and exercise objectivity and professional skepticism this guide is designed to help you understand independence requirements under the aicpa code of professional conduct and if applicable other rule making and standard setting bodies. 2 representing facts truthfully in reports and discussions. December 15 2014 using content in the online system as of august 31 2016 december 15 2014 using content in the online system as of june 21 2016 december 15 2014 using content in the online system as of october 26 2015. Cathy allen cpa formed audit conduct llc in 2005 to help cpa firms comply with an array of auditor independence and professional ethics rules.

Uniquely experienced she develops numerous aicpa courses on professional ethics independence and related topics provides specialized training and advises firms on critical independence matters and quality controls.

Module B Professional Ethics Ppt Download

User Friendly Aicpa Code Of Ethics On Horizon

Aicpa Conceptual Framework Approach

Https Www Aicpa Org Content Dam Aicpa Interestareas Professionalethics Resources Tools Downloadabledocuments Plain English Guide Pdf

Ethics Real Life Application Of The Aicpa Code Of Professional Condu

Professional Conduct Independence And Quality Control Ppt Video Online Download

Comparing The Ethics Codes Aicpa And Ifac

Solved The Aicpa Code Of Professional Conduct Rules Of Co Chegg Com

Integrity Objectivity And Independence Core Elements Of The Aicpa Code Of Professional Ethics Jane Zhang Assistant Professor And Debra M Grace Professor Ppt Download

Ethics Real Life Application Of The Aicpa Code Of Professional Condu

A New Take On Ethics And Independence Journal Of Accountancy

Ppt Integrity Objectivity And Independence Core Elements Of The Aicpa Code Of Professional Ethics Powerpoint Presentation Id 7066114

Professional Ethics What Are We Not To Do Ppt Download