Aicpa Code Of Professional Conduct

Aicpa Code Of Professional Conduct

User Friendly Aicpa Code Of Ethics On Horizon

User Friendly Aicpa Code Of Ethics On Horizon

Ethics Real Life Application Of The Aicpa Code Of Professional Condu

Ethics And Professional Conduct For Cpas

Purpose And Content Of The Aicpa Code Of Professional Conduct Youtube

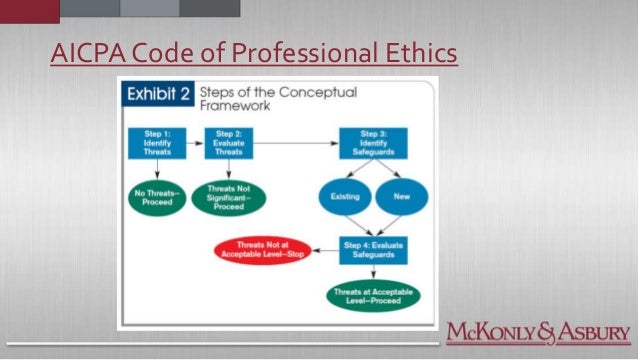

0 200 020 application of the aicpa code 01 the code of professional conduct the code was originally adopted on january 12 1988 and was periodically revised through june 1 2014.

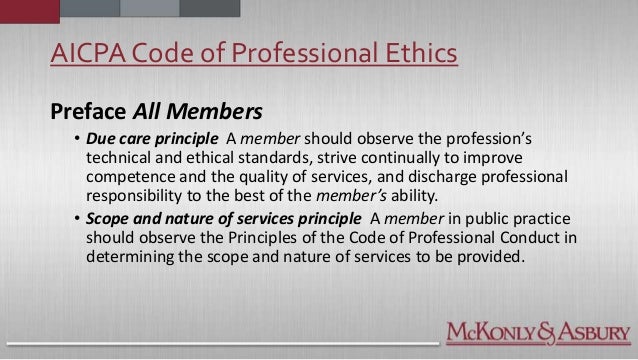

Aicpa code of professional conduct. The code of professional conduct was revised effective december 15 2014. The american institute of certified public accountants aicpa has outlined the expected code of conduct for accounting professionals. The aicpa code of professional conduct is a collection of codified statements issued by the american institute of certified public accountants that outline a cpa s ethical and professional responsibilities. The first ethical guidance members and all cpas should look to is the ethical requirements of their state cpa society and or state board of accountancy.

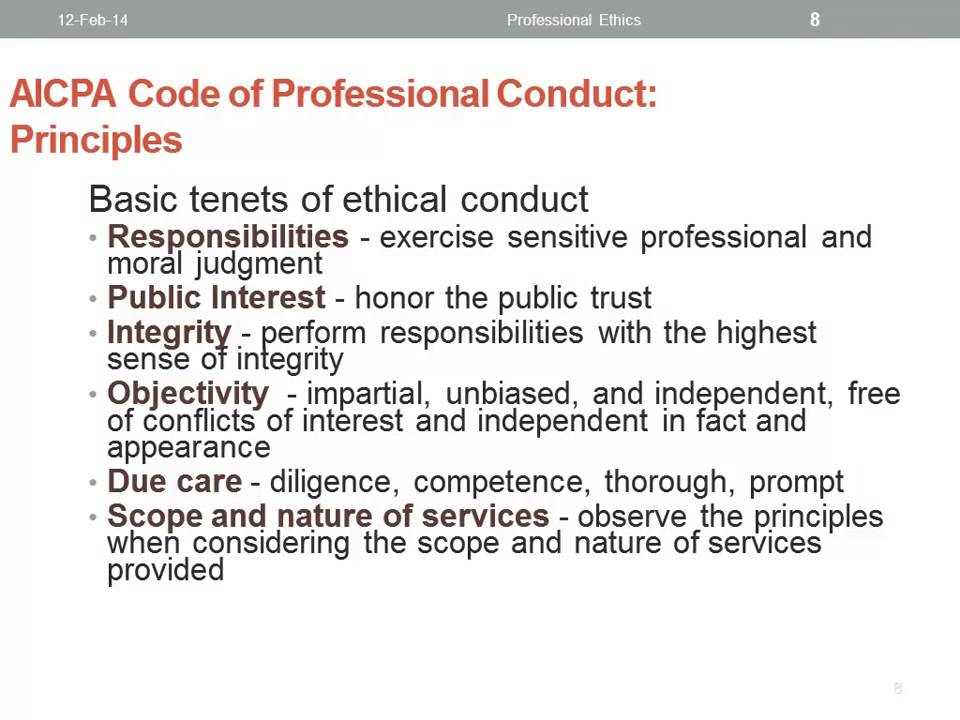

The aicpa a code of professional conduct is meant to be a general framework but there are several governing bodies that need to be considered when we approach the topic of ethics. The aicpa code of professional conduct provides guidance and rules to all members in the performance of their professional responsibilities. The code establishes standards for auditor independence integrity and objectivity responsibilities to clients and colleagues and acts discreditable to the accounting profession. On june 1 2014 the aicpa issued a codification of the code s principles rules interpretations and rulings revised code.

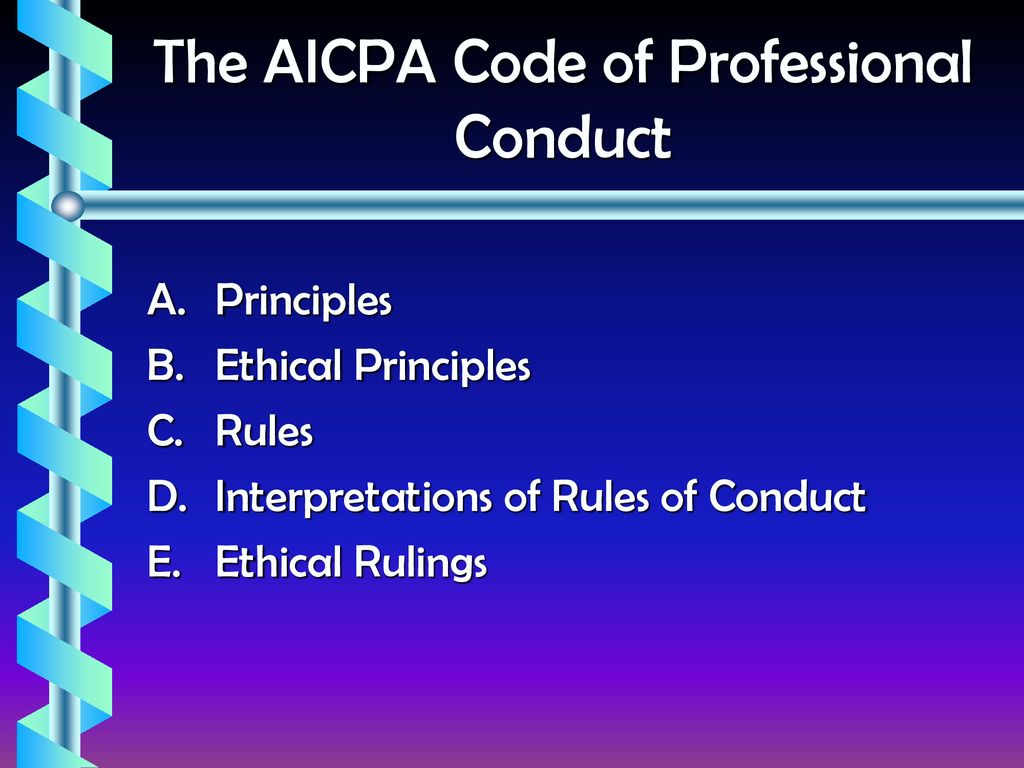

The american institute of certified public accountants aicpa takes ethics and professional conduct very seriously. It is indeed considered to be the backbone of ethical reasoning in the field of accounting. The code consists of principles and rules as well as interpretations and other guidance. A national effort is underway to encourage more state boards of accountancy to adopt the.

Learn more about the project that resulted in the redesigned code of professional conduct.

Code Of Professional Conduct Ppt Download

Independence Aicpa Code Of Professional Conduct Article Iv Ppt Video Online Download

Ethics Real Life Application Of The Aicpa Code Of Professional Condu

Https Www Aicpa Org Research Standards Codeofconduct Downloadabledocuments 2014december15contentasof2016august31codeofconduct Pdf

Basic Tenets Of Ethical Conduct In Auditing Youtube

Solved Statements Answer 1 The Aicpa Code Of Professiona Chegg Com

Aicpa Code Of Professional Conduct Answers To Your Ethical Questions Cpa Hall Talk

.jpg)

Aicpa Code Of Professional Conduct

Solved Aicpa Professional Code Of Conduct Read The Overvi Chegg Com

Professional Ethics What Are We Not To Do Ppt Download

Pdf Ethical Exemplification And The Aicpa Code Of Professional Conduct An Empirical Investigation Of Auditor And Public Perceptions

The Aicpa Code Of Professional Conduct What You Need To Know Cpa Self Study Self Study Cpe For Cpas

Aicpa S Code Of Professional Conduct